After years of modest increases, the number of cut flower growers in the United States surged 64% between 2019 and 2024, even as broader floriculture sales growth remained largely flat.

The number of cut flower growers rose from 2,035 in 2019 to 3,347 in 2024, according to data released in February from the U.S. Department of Agriculture’s 2024 Census of Horticultural Specialties.

The increase was driven largely by smaller farms. Growers reporting less than $100,000 in annual sales more than doubled since 2019, increasing 107% from 811 operations to 1,678. Growers reporting sales $100,000 or more grew 30%, from 267 in 2019 to 346.

Despite the surge in growers, total sales grew at a slower pace. Cut flower sales rose 22% between 2019 and 2024, reaching $468 million, the census found. But that growth looks different when viewed against broader economic trends.

That’s because from 2019 to 2024, the Consumer Price Index increased 22.6%, suggesting that total floriculture industry sales “just kept pace” with inflation, says Marvin Miller, Ph.D., AAF, of Ball Horticulture, who analyzes industry data.

Still, the increase represents a recovery from the drop in the USDA’s 2019 Census of Horticultural Specialties, which is conducted every five years. It found that from 2014 to 2019, sales declined 14.7%, from $452 million to $385 million. Adjusted for inflation during that period, sales declined by about 21%.

Separately, the USDA’s 2024 Floriculture Crops Summary shows the number of U.S. floriculture producers increased to 11,262 in 2024, up from 10,216 in 2023 — a gain of more than 1,000 operations — while total floriculture sales reached $6.71 billion, up less than 1% from the previous year.

The census and floriculture crops summary datasets are not directly comparable — the census captures all U.S. operations every five years, while the annual floriculture survey focuses on sales and production in the top-producing states. Together they offer a more complete picture of the industry.

More small growers enter the market

The surge in cut flower growers is one of the largest gains for any segment in the horticulture industry, which includes nursery stock, bedding and garden plants, sod, foliage plants, propagative materials and other specialty crops.

The growth builds on a longer-term trend: there were 1,703 cut flower growers reported in the 2009 census and 1,998 growers in the 2014 census.

“We have seen a resurgence in growers, but it’s the smaller, local growers,” says Lane DeVries, AAF, executive director of CalFlowers (the California Association of Flower Growers & Shippers) and former owner of Sun Valley Floral Farms. “There’s a huge surge of small, local flower farmers throughout the country.”

While the number of smaller growers is rising rapidly, their impact on total sales remains less clear, as production — and revenue — continues to be concentrated among larger commercial operations.

Cut flowers show stronger growth among larger growers

At the same time, sales trends tell a more nuanced story. Within the broader floriculture category, cut flowers posted stronger gains among larger commercial operations.

Sales among growers with $100,000 or more in revenue rose to $414 million in 2024, up from $350 million in 2023 — an increase of more than 18%.

Over the 2019–2024 period, cut flower sales grew 22%, while overall floriculture sales were essentially unchanged year over year.

Top flower producing states

California retained its status as the top state for cut flower growers and gained more than 100 additional growers (a 44% increase), according to the census. Michigan ranked second, rising from fourth in the 2019 census — and more than doubling the number of producers from 135 to 308. Rounding out the top five were Washington, New York and Pennsylvania.

Hawaii, the second-highest cut flower grower in 2019, lost 70 growers, falling to ninth in the 2024 census. It was one of eight states whose grower numbers decreased, including Alaska, Arizona, Arkansas, Maine, Montana, Nevada, and Oregon.

Smaller markets gain ground

California has held the largest share of domestic flower sales for decades, but its dominance has steadily declined over the past 10 years. According to the 2014 census, California accounted for 74% of nationwide cut flower sales. That share fell to 66% in 2019, and to 53% in 2024.

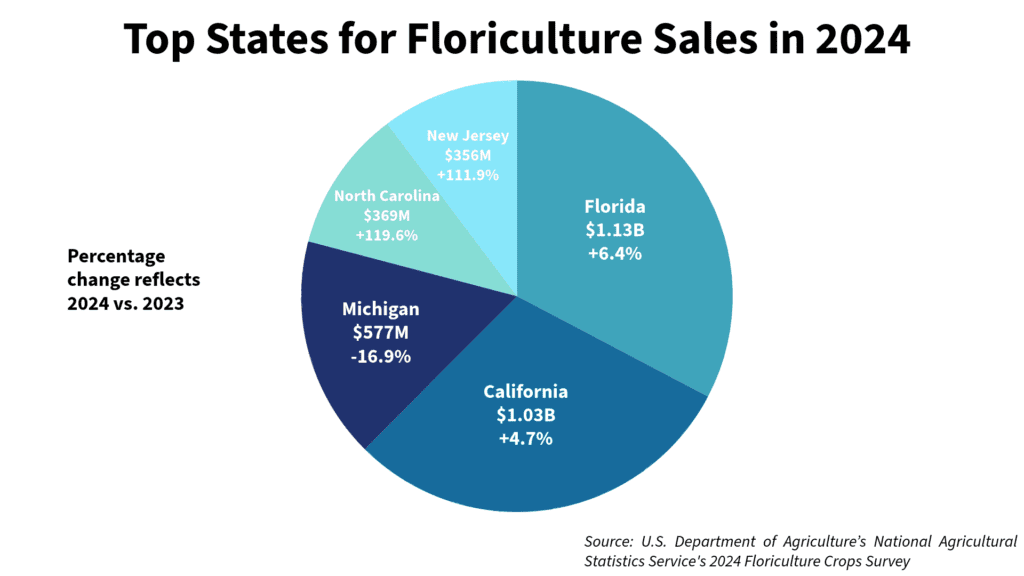

At the same time, floriculture sales remain concentrated among a handful of states. Florida and California led the nation in 2024, generating $1.13 billion and $1.03 billion in sales, respectively, followed by Michigan, North Carolina and New Jersey.

DeVries attributes the decline, in part, to a nationwide shift toward locally sourced flowers, a trend that echoes the era before industrialization and improved shipping enabled the consolidation of large-scale California production.

“The small farms across the country are regaining market share because they’re supplying their cities,” he says. “150 years ago, flower production happened all around the cities. We’re going back to how it started.”

Sales of cut greens decline

Cut greens sales fell 19% from nearly $100 million in 2019 to $81 million in 2024 — a roughly one-third decline after adjusting for inflation. The number of operations slipped slightly to 617, continuing a longer-term decline from 728 in 2014.

Florida remains the dominant producer but has seen sharp losses, with growers down 41% since 2014. Other states, including Virginia, North Carolina, Hawaii and Maryland, also reported significant declines.

Industry leaders point to rising imports, increasing costs and land values, and generational transitions as key factors.

“You have imports keeping pressure on prices while costs keep going up,” says David Register of FernTrust. “And in places like Florida, land values have risen so much that growing cut greens often doesn’t make economic sense anymore.”

At the same time, production is shifting geographically, with 23 states reporting increases, led by Utah, New Jersey and Texas.

Laurie Herrera is a contributing writer for the Society of American Florist.